CFOs – a game-changing new judgment

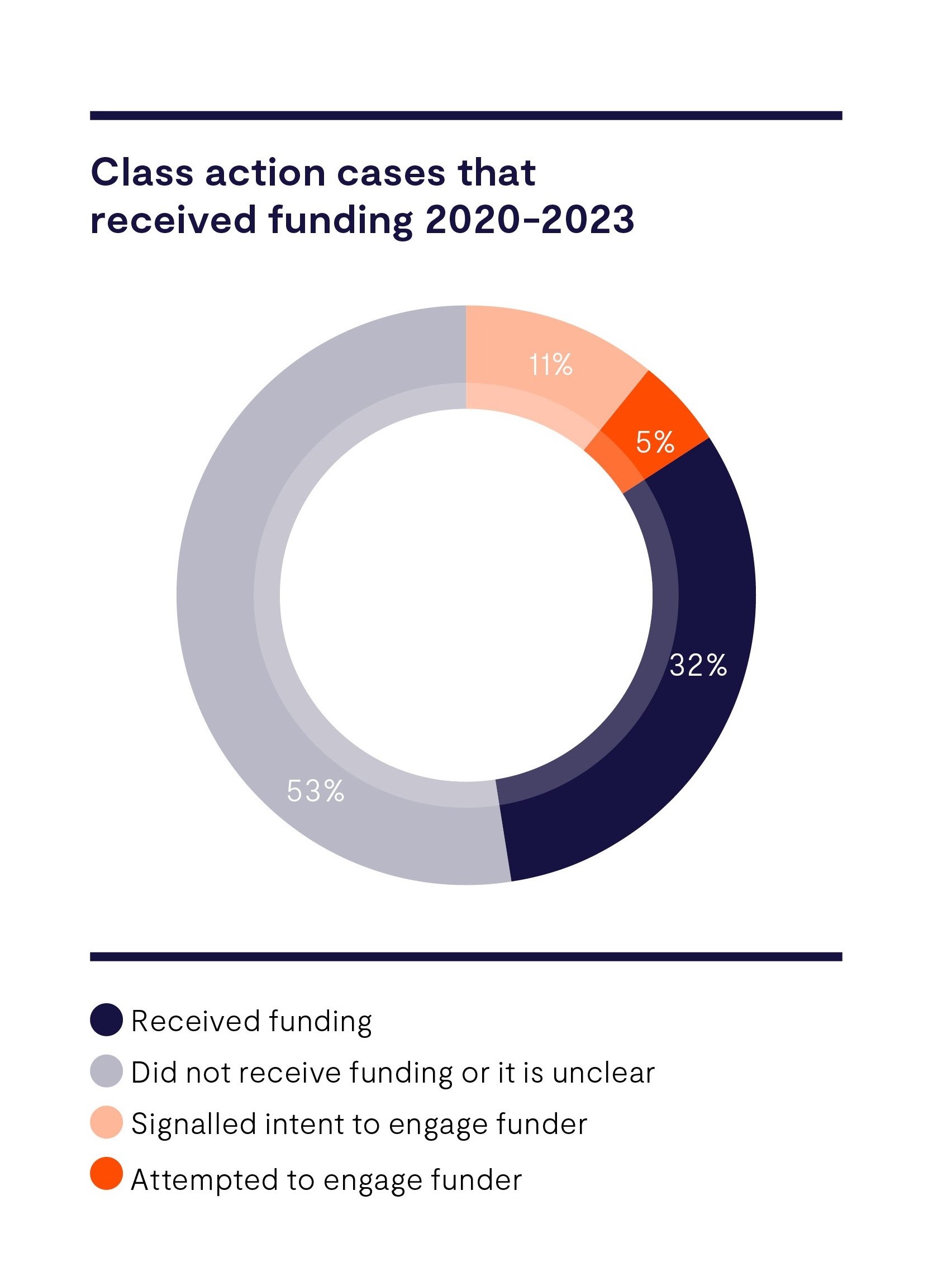

The majority of class actions are not currently funded. That may start to change.

In the recently released Simons v ANZ and ASB judgment,2 the Court of Appeal confirmed the courts have jurisdiction to make common fund orders (CFOs). CFOs impose the contractual terms of the funding arrangement between the representative plaintiff and the litigation funder on all members of the class – preventing the “free rider” behaviour that can otherwise occur in opt-out class actions. The Court of Appeal agreed with the High Court’s decision that the High Court Rules are broad enough to enable the court to issue a CFO, and went further, saying these could be granted at an early stage of the proceeding.

The Court of Appeal found the commercial viability of a litigation funding arrangement enhances access to justice by providing certainty in how representative proceedings are funded. This would: “ensure the benefits of a successful representative proceeding is shared fairly between the representative plaintiff and all class members. Access to justice is best enhanced through the allocation of the fruits of a successful representative proceeding being agreed upon at an early juncture”, giving litigation funders comfort that they will receive a return on their investment if the case succeeds.