Chapman Tripp analysis

Our review of CRDs published to date shows a wide range of reporting styles, and significant variation in the depth of reporting content. The banking and financial services sector has tended to produce more detailed reports, alongside detailed reporting from the energy sector. Listed issuers range significantly depending on the significance of climate change for the relevant business, with some issuers presenting less sophisticated reports and omitting mandatory reporting requirements, including metrics.

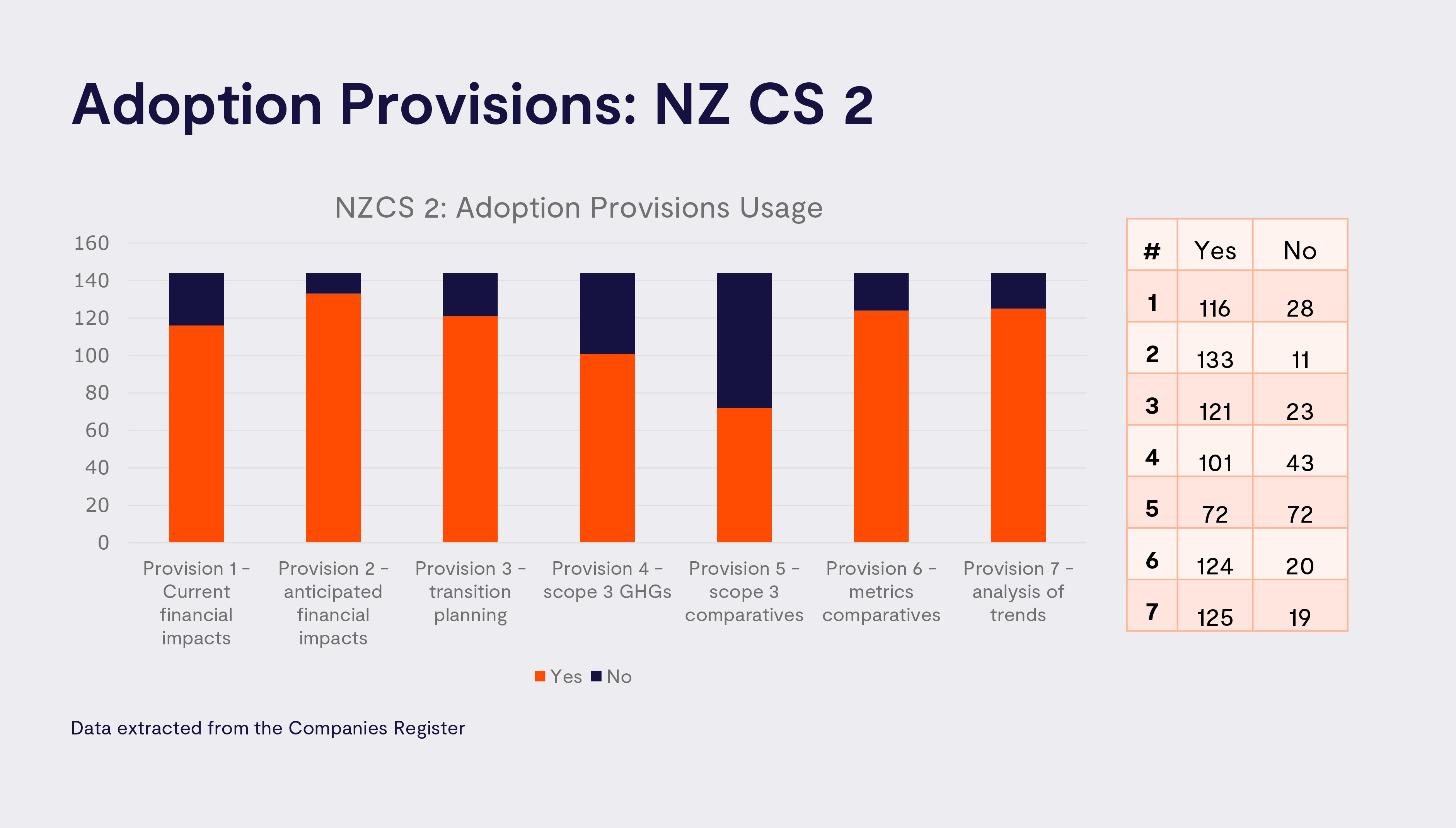

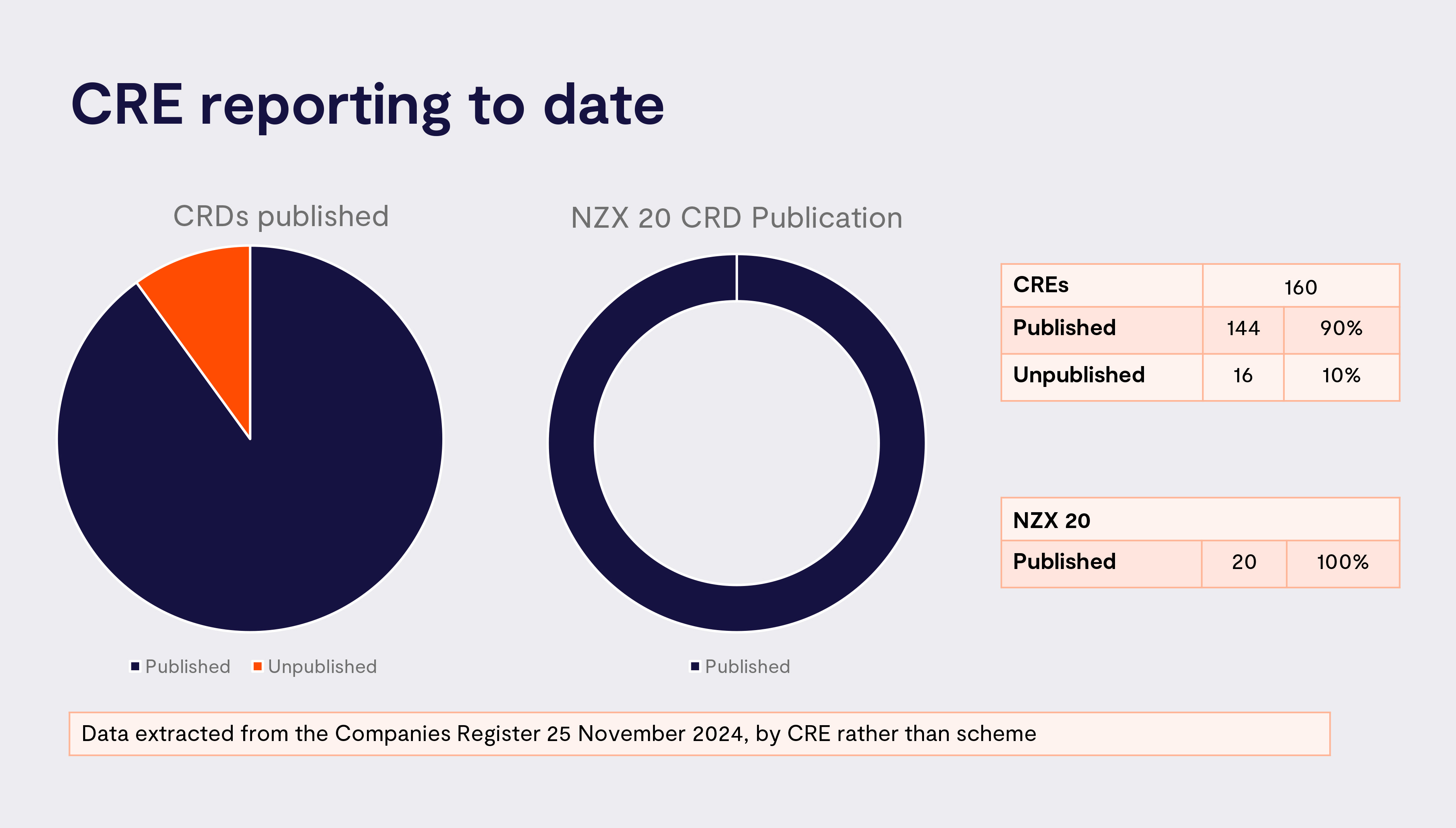

Our analysis shows that CRD published by late November (representing 90% of all CREs) demonstrated strong uptake of adoption provisions across the board, even where relevant content could be (or was) provided. Unsurprisingly, the highest use of any adoption provision was in relation to AP 2 to defer disclosure of anticipated financial impacts (see Figure 1). There was also strong uptake of the adoption provision relating to transition planning (with 84% of CREs utilising adoption relief for this disclosure requirement), which reflects the lack of detailed NZ-specific guidance on this key topic in FY24. The average length of first year CRD reports was just over 41 pages – in general, mandatory CRD reports were shorter and more concise than voluntary climate reports published in FY23.

CREs have generally published their CRD separately to their annual reports or sustainability reports, and many CREs took the full four-month period beyond their annual report publication date to publish their CRD.

Some general themes emerge from a survey of published FY24 CRDs:

- For the Governance section of NZ CS 1, CRDs showed a tension between processes and mechanisms set out in Board or Committee Charters (ie what ‘usually’ happens, or is mandated to occur), and actions that actually took place in the relevant reporting period – reflected in the FMA’s feedback on this point above.

- Strategy disclosures demonstrated a stronger and more granular understanding and analysis of physical risks and impacts relative to transition risks and impacts, which demonstrated variability, particularly in relation to emerging risks. Scenario analysis disclosures showed sophistication, which reflected the work many CREs had undertaken to prepare for earlier voluntary disclosures, and scenarios constructed at the sector level. While the focus in Year 1 was on conducting a scenario analysis for the first time, we expect that going forward CREs will need to ensure their scenarios are appropriately challenging, in line with FMA indications, and that insights from this process are integrated into business planning, not left to one side.

- Risk Management disclosures showed that the maturity and integration of climate risk was highly variable between CREs, with many reporting standalone climate risk identification and assessment process that are not yet integrated into broader risk management reporting or outputs – such as asset management and business planning.

- In Metrics and Targets disclosures, many CREs experienced challenges with disclosing vulnerability metrics, in part due to “vulnerability” not being defined in the NZ CS, and challenges related to commercial sensitivity. CREs are communicating GHG emissions targets in increasingly nuanced ways, including by differentiating between near-term targets and longer-term (2050) aspirations or ambitions. This in part reflects the changing risk environment relating to climate targets (see our separate publication on this point here).

Primary user feedback

The FMA’s monitoring report is accompanied by primary user feedback starting to enter the market. Forsyth Barr has taken the lead in publishing sectoral analyses of climate statements, to date covering the aged care and electricity sectors, which have identified a number of key areas for improvement in FY25, including the need for CREs to provide information about issues which have the potential to impact shareholder value over time. In particular, Forsyth Barr noted that robust quantification of impacts will be most useful for investors to make assessments between entities and over time. Forsyth Barr also noted that CREs could improve disclosures on business continuity planning in the context of identified climate related risks. Forsyth Barr encouraged “evolution towards emerging best practice where transition plans include time bound, [quantitative] data designed to show how a company plans to deliver on its emissions reduction targets”.

Global developments

Panning out to a global view, the climate reporting landscape continues to evolve. The International Sustainability Standards Board (ISSB) estimates that 55% of global GDP is now covered by ISSB-aligned standards, whether in force or proposed.

Mandatory CRD on the rise in New Zealand’s key export markets

Our April report for The Aotearoa Circle identified that c. 80% of New Zealand exports by value are going to countries with mandatory CRD in force or proposed. This figure increased to 85% for the June 2024 quarter, driven in part by new export partners introducing ISSB-aligned disclosure requirements, including the Republic of Korea.

New Australian CRD regime effective 1 January 2025

Australia’s Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 received Royal Assent on 17 September 2024, amending the Corporations Act 2001 to require sustainability reporting. The mandatory climate-related disclosures are set out in Standard AASB S2 issued by the Australian Accounting Standards Board (AASB). The Board has also issued a voluntary standard for sustainability-related disclosures, AASB S1. These are respectively aligned to the ISSB Sustainability Disclosure Standards IFRS S2 and IFRS S1, with some modifications to reflect the Australian context.

Sustainability reporting requirements for the largest entities will come into force for financial years commencing from 1 January 2025. The reporting requirements will then be implemented on a staged basis through to FY28.

Key differences between the Australian and New Zealand CRD requirements are below:

- Scope: Australia’s regime applies to all large entities required to prepare financial reporting under the Corporations Act 2001, with ‘Group 1’ entities (captured from 2025) being those meeting two of three of ≥$AU500m in consolidated revenue; ≥$1b EOFY consolidated gross assets; or ≥500 employees. The Australian scheme will therefore capture large private entities as well as the large listed issuers, fund managers, banks and insurers that are within scope of the New Zealand regime.

- Assurance: The Australian regime will require assurance over the whole of a sustainability report by 2030, which is much more extensive than the New Zealand requirement to assure solely the GHG emissions disclosures. The assurance requirements will be phased in, with the timeframe to be confirmed. The Australian Auditing and Assurance Standards Board has issued an exposure draft of a proposed standard on the timeline for audit and review of sustainability reports and is currently considering feedback from submitters.

- Liability regime: Unlike the New Zealand regime, there is no deemed liability for directors for failure to comply with the mandatory reporting requirements. In addition, for the first reporting year, CREs and directors have a limited immunity in respect of all “future” climate-related statements. For the first, second and third reporting years, CREs and directors have a limited immunity in respect of scope 3 GHG emissions, scenario analysis and transition planning disclosures. The immunity does not apply to criminal proceedings, or proceedings brought by the Australian Securities & Investments Commission.

- Smaller entities are able to disclose that they have no material financial climate-related risks or opportunities, rather than producing a full sustainability report.

- The Australian legislation requires analysis of two scenarios, rather than three.